The Dutch private capital market reflected a quarter of contrasts in Q2 2025, as investors and companies navigated macroeconomic uncertainties stemming largely from global tariff tensions.

Overall, deal activity in both venture capital and private equity declined compared to previous quarters.

However, late in the quarter, signs of recovery emerged, particularly in private equity, indicating a more optimistic outlook for the second half of the year.

Contentlockr

Additionally, public equity markets demonstrated resilience, and deal-making in certain sectors continued to remain active.

The latest data from PitchBook’s Q2 2025 Netherlands Market Snapshot provides an in-depth view of these shifting dynamics.

Here are the key takeaways:

Maintained a steady economic growth

In Q2 2025, the Dutch economy maintained a steady growth pace, with GDP expanding by 1 per cent QoQ.

This performance was driven by exports, which saw a boost from increased manufacturing activity.

Inflation decelerated in June to 3.1 per cent, with tobacco having a negative effect on inflation due to the excise duty hike implemented in April 2024.

This increase was part of the Dutch government’s broader “National Prevention Agreement,” which aims to create a tobacco-free generation by 2040. On the contrary, flight tickets exerted downward pressure on inflation due to a year-over-year price drop.

Unemployment in the Netherlands stood at 3.8 per cent, making it one of the lowest in the EU. The euro experienced an appreciation against the US dollar, driven by a weakening dollar amid tariff negotiations.

The European Central Bank cut rates twice in Q2, while the US Federal Reserve kept its interest rates unchanged.

AEX recovers after tariff shock

Q2 was an unusual quarter for public markets, starting with global tariff announcements on “Liberation Day,” April 2.

Markets around the world fell sharply, with the AEX index dropping by as much as 13 per cent after the US announced a 20 per cent tariff on the European Union.

However, a 90-day pause in implementing the tariffs later eased market concerns, suggesting the announcement was mainly a negotiation tactic by the US.

By the end of Q2, the AEX had recovered to its Q1 levels. The impact of the potential US tariffs varied among Dutch companies.

While consumer staples like Unilever struggled to recover, tech and financial stocks such as ING, Adyen, and ASML saw their share prices increase. For more details, check out our analyst note, “The Impact of Tariffs on European PE.”

In Q2, there was only one public listing in the Netherlands: Triodos Bank, which listed on Euronext Amsterdam with a market cap of €434M.

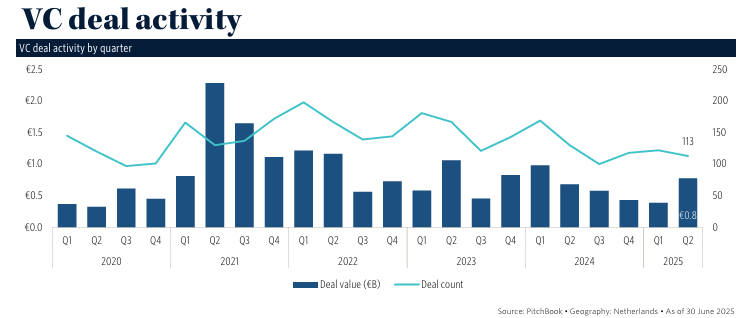

VC investment grows but lags at exit activity

Venture capital deal value rebounded in Q2, although deal count remained slightly subdued. Expectations for improved activity in H2 remain high as market conditions stabilise.

More than half of Q2’s deal value stemmed from nontraditional investors participating in VC rounds.

For example, Toloka AI raised €64M from Jeff Bezos’s family office and Spotify’s CTO, Mikhail Parakhin. Notably, more than 50 per cent of Q2 VC deal value came from late-stage rounds.

VC exits in the Netherlands remained sparse, with just eight exits totalling under half a billion euros. Seven of those exits came from the IT sector.

On the fundraising front, VC activity stayed notably low year-to-date, with only three new funds closing. Nonetheless, venture capital AUM in the Netherlands continued to grow, expanding the dry powder available in the country.

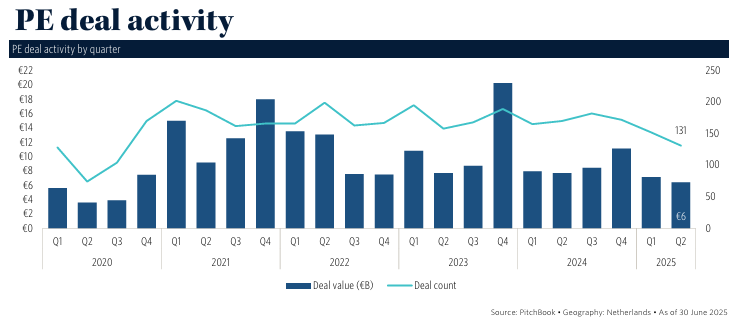

PE deals slow but pick up late in the Quarter

Dutch private equity deal activity declined significantly in Q2, raising €6B across only 131 deals, one of the lowest quarterly counts in the last five years.

Dealmaking stalled at the start of the quarter in response to the US tariff announcement, which created considerable uncertainty.

However, according to PitchBook, the latter part of Q2 showed a clear ramp-up in activity, as documented in their Q2 2025 European PE Breakdown report.

The largest PE deal during Q2 was a €300M investment in SkyNRG by APG. Founded in 2009 by KLM Royal Dutch Airlines, SkyNRG is active in the sustainable aviation fuel (SAF) industry. This capital injection will support SkyNRG’s expansion into new SAF production facilities in the Netherlands, Sweden, and the US.

PE exit activity rebounded in Q2 from a deal count perspective, though the overall exit environment remained constrained due to macroeconomic challenges and valuation mismatches.

The largest exit year-to-date involved the sale of LBC Tank Terminals to Mitsui O.S.K. Lines for €1.6B, allowing French PE firm Ardian to exit its investment after holding its stake since 2017.

Fundraising stays low

On the fundraising front, private equity saw five new funds raise under a combined €2B in the first half of 2025.

Notably, 90 per cent of the capital raised came from buyout strategies. The standout in this category was Egeria, which raised €1.3B for its sixth fund, accounting for the bulk of capital raised in the Netherlands this year.

Despite a dip in new fundraising, the Netherlands’ PE asset under management remains healthy, with total AUM just shy of €50B. This sustained capital base provides dry powder that could help reaccelerate dealmaking as macroeconomic headwinds ease.

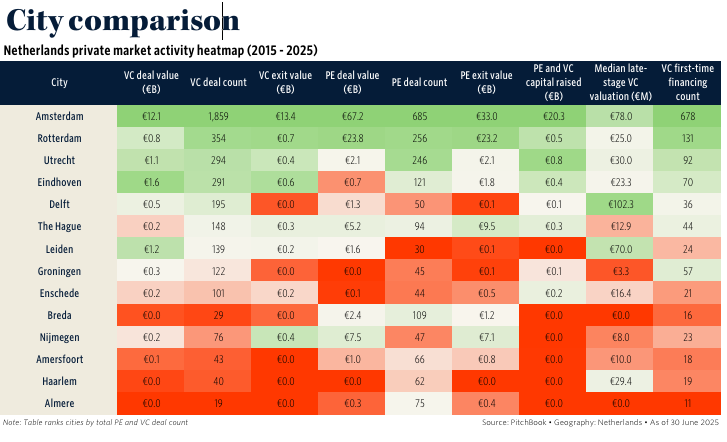

Amsterdam maintains dominance

The city comparison heatmap in the report highlights Amsterdam’s leading position in the Dutch private capital ecosystem.

Since 2015, Amsterdam has recorded €12.1B in venture capital (VC) deal value and €67.2B in private equity (PE) deal value, substantially surpassing other cities like Rotterdam, Utrecht, and Eindhoven.

While hubs such as Delft, Leiden, and Groningen have contributed to deal activity at lower levels, they have demonstrated significant involvement in specific sectors, especially in academia and health tech.